Ready in minutes

AI builds your ad from a single prompt

July 07, 2025

Disney+ captures 1.9% of total TV viewing. Here's how to reach its family audience.

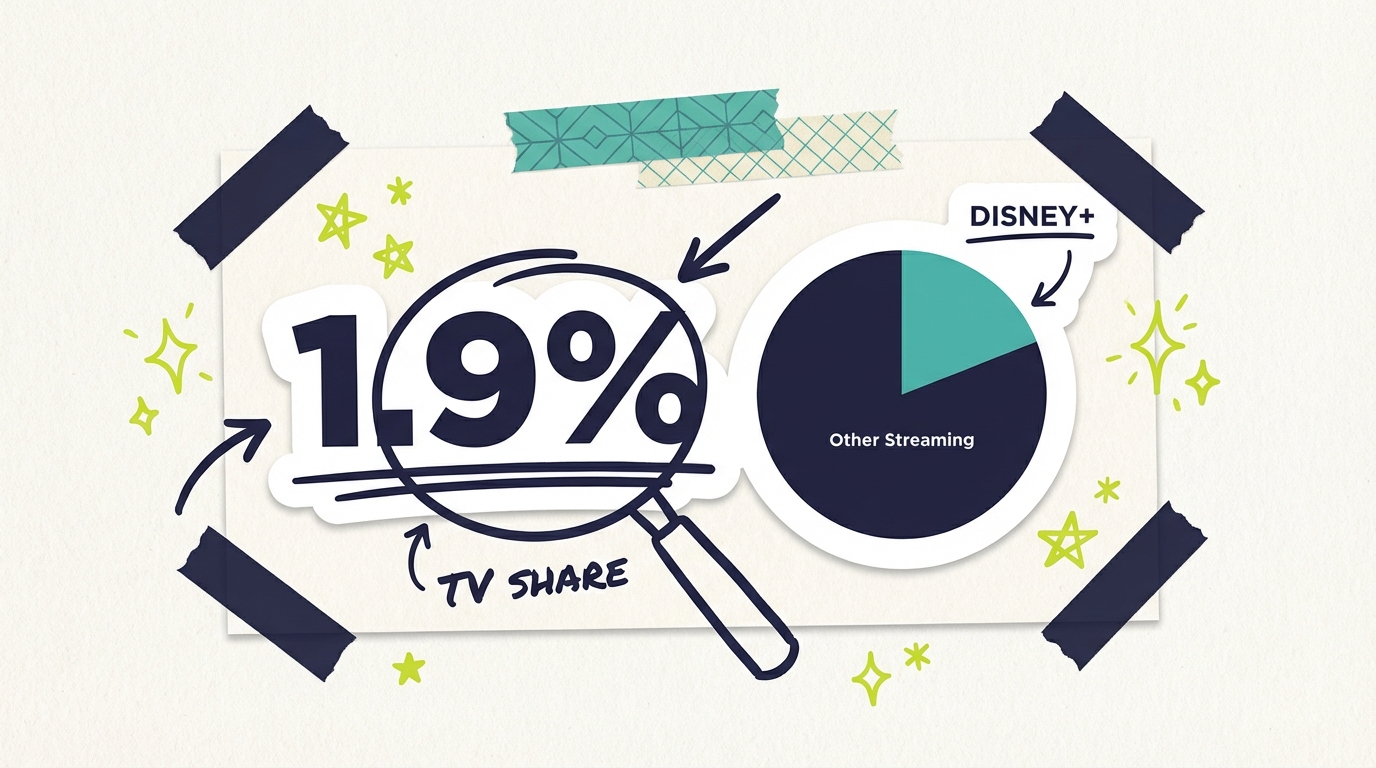

1.9%

Disney+'s share of total TV viewing (2025)

11.2%

Disney company's total TV viewing share (Dec 2024)

120M

Global Disney+ subscribers (mid-2025)

Disney+ captures approximately 1.9% of total television viewing in the United States as of mid-2025, according to Nielsen's monthly Gauge report. While this percentage may seem modest compared to streaming giants like YouTube at over 10% and Netflix at 7-8%, Disney+ has carved out a valuable niche with family-friendly content that drives high engagement and strong advertiser appeal among audiences that are notoriously difficult to reach through other channels.

Understanding Disney+'s position in the streaming landscape helps businesses evaluate their television advertising options and identify opportunities to reach specific audience segments. The service's unique content library, particularly its dominance in children's programming and its exclusive access to Marvel, Star Wars, and Pixar franchises, creates specific audience reach opportunities that differentiate it from general-entertainment streaming platforms competing for the same viewing time.

Nielsen's comprehensive TV measurement reveals Disney+ holding steady around 1.8-2.0% of total television viewing throughout 2024 and into 2025, showing remarkable consistency despite the volatile streaming market. This share places Disney+ in the middle tier of streaming platforms, typically ranking as the fifth or sixth largest streaming service by viewing time behind YouTube, Netflix, Amazon Prime Video, and often Hulu, which Disney also owns and operates as part of its broader streaming strategy.

The Disney+ viewing share represents a remarkable achievement considering the service launched only in November 2019, giving it less than six years to establish this market position. Within five years, Disney+ grew from zero to capturing nearly 2% of all American television viewing, demonstrating the power of Disney's content library and brand recognition to attract and retain subscribers in a crowded streaming marketplace. Few media companies have built such significant viewing share so quickly from a standing start.

Disney+'s share shows seasonal patterns tied to content releases that create predictable viewing fluctuations throughout the year. Major franchise releases like Marvel series, Star Wars shows, and Pixar films create viewing spikes that can temporarily push Disney+ above 2% of total TV as fans tune in for premiere episodes and word of mouth drives additional viewers to catch up. Conversely, periods between major releases see the platform's share dip toward 1.7-1.8% as families exhaust the catalog content they want to watch and wait for the next major premiere.

The service's content strategy heavily emphasizes franchises and family programming rather than attempting to compete across all genres like broader platforms such as Netflix or Amazon. "Bluey," the Australian animated series, has become a phenomenon on Disney+ that extends far beyond its original children's audience, regularly ranking among the top streaming titles across all platforms regardless of genre or target demographic. During December 2024, Bluey accumulated 5.3 billion viewing minutes, ranking as the second most-watched streaming title of the month and demonstrating the power of must-watch children's content to drive platform engagement.

Disney+ has expanded into ad-supported streaming by launching its ad tier in December 2022, fundamentally changing the platform's value proposition for both consumers and advertisers. This move opened the platform to advertisers for the first time and brought more price-conscious subscribers onto the service who had previously been priced out of Disney+'s premium positioning. The ad-supported tier has grown to represent a significant portion of Disney+ subscriptions, creating advertising inventory that wasn't previously available and enabling brands to reach Disney's valuable family audience through television commercials.

It's worth noting that Nielsen's viewing share for Disney+ counts only the Disney+ streaming app itself, not Disney's broader media portfolio. The broader Disney company, including its cable networks ESPN, FX, and Freeform along with broadcast properties like ABC, commands approximately 11% of total TV viewing according to Nielsen's Media Distributor Gauge. This makes Disney the largest media company by viewing share, demonstrating how Disney+'s streaming service fits within a much larger entertainment ecosystem that spans traditional and digital platforms.

Disney+'s nearly 2% share of viewing represents millions of highly engaged viewers, many of them families with children who are notoriously difficult to reach through other advertising channels. This audience concentration creates unique value for advertisers targeting parents, children, and household decision-makers who control spending on everything from groceries to vacations to educational products.

The platform's audience demographics skew toward families and younger viewers in ways that differentiate Disney+ from general-entertainment streaming services. Households with children over-index dramatically on Disney+ usage compared to general streaming platforms, creating efficient reach for advertisers targeting parents and kids. This makes Disney+ particularly valuable for businesses targeting parents, family services, children's products, and household goods that benefit from reaching decision-makers in family contexts.

For advertisers, Disney+'s ad-supported tier has opened access to premium content in a brand-safe environment that eliminates many concerns associated with advertising on user-generated content platforms. Disney maintains strict content standards across its platforms, ensuring advertisers won't appear alongside controversial or inappropriate content that might create brand safety issues. This brand safety premium comes built into Disney+ advertising without additional vetting, monitoring, or brand safety technology that would add cost and complexity to campaigns on other platforms.

The quality of Disney+ content also translates to advertising effectiveness in ways that matter beyond simple reach metrics. Viewers actively choose to watch Disney+ programming rather than passively consuming whatever appears in their feed, creating intentional viewing behavior that generates higher engagement and attention for advertising messages. When a family sits down to watch Disney+ together, they're making a deliberate choice that indicates engagement levels superior to background viewing or passive content consumption.

Small businesses considering television advertising can access Disney+ inventory through platforms like Adwave, which includes Disney+ among its 100+ premium channels. Starting at just $50, businesses can reach Disney+ viewers alongside audiences on other major streaming platforms without negotiating separate deals with Disney or meeting high minimum budgets that would otherwise make Disney+ inaccessible to smaller advertisers.

Understanding Disney+'s share requires context about Disney's broader streaming strategy, which includes multiple services targeting different audiences and creating a comprehensive ecosystem that competes with Netflix and other standalone platforms. Disney's approach involves portfolio management across services rather than consolidating everything into a single app.

Disney+ focuses on family entertainment, including Disney animated films, Pixar, Marvel, Star Wars, and National Geographic content that appeals to specific audience segments rather than attempting to serve all viewers. The service targets families, children, and fans of Disney's major franchises who want deep libraries of content within these verticals. Subscriber counts have fluctuated as Disney experimented with pricing and content strategies, reaching approximately 120 million subscribers globally by mid-2025 after earlier peaks above 130 million.

Hulu, which Disney fully controls after acquiring Fox's stake in 2019, targets adult audiences with general entertainment programming that Disney+ doesn't carry. Hulu's content library includes original series, network TV content from partners, and movies that appeal to adults who watch more television overall than children and families. Hulu captures approximately 3.4% of total TV viewing, significantly more than Disney+, partly because its content library appeals to adult viewers who have more available viewing time and watch more hours of television per week.

ESPN+ rounds out Disney's streaming portfolio by focusing on live sports not available on ESPN's linear channels, providing a streaming home for sports fans who want to follow niche sports, college athletics, and events that don't make ESPN's broadcast schedule. While smaller than Disney+ and Hulu in total viewing share, ESPN+ attracts highly engaged sports fans willing to pay for premium content and tolerant of advertising that's been part of sports broadcasting for decades.

Disney has increasingly bundled these services together, offering discounts for subscribers who take all three platforms and simplifying the value proposition for households that want comprehensive entertainment options. This bundle strategy aims to reduce churn by creating multiple reasons to maintain subscriptions and increase total household engagement with Disney's streaming ecosystem across family viewing, adult entertainment, and sports.

Combined, Disney's streaming services Disney+, Hulu, and ESPN+ capture approximately 6-7% of total TV viewing, making the bundle comparable in scale to Netflix when considered as a unified offering. This combined approach allows Disney to offer advertisers reach across family, general entertainment, and sports audiences through a single sales relationship, competing effectively with Netflix's broader positioning.

Disney+'s viewing patterns reflect its unique content positioning in the streaming market, with different content categories driving viewing at different times and creating distinct opportunities for advertisers seeking to reach specific audiences.

Children's programming drives substantial viewing on Disney+ throughout the day, creating a reliable base of engagement that persists regardless of major release schedules. Shows like "Bluey," "Mickey Mouse Clubhouse," and classic Disney animated content generate consistent daily viewing from families with young children who rely on Disney+ as a safe, trusted entertainment source. This children's viewing often occurs during daytime hours when parents use television to occupy kids, creating advertising opportunities during underutilized dayparts when CPMs are lower and frequency is more affordable.

Marvel and Star Wars franchises create viewing events around premiere dates that attract adult audiences beyond Disney+'s family core and generate significant attention in entertainment media. New episodes of series like "Loki," "The Mandalorian," or "Ahsoka" generate significant premiere-week viewing that rivals or exceeds typical cable series audiences, with social media conversation amplifying awareness and driving additional sampling. These franchise releases temporarily boost Disney+'s viewing share and create opportunities for advertisers seeking to align with cultural moments and passionate fan communities.

Disney's theatrical releases transition to Disney+ after theatrical windows, creating extended viewing opportunities that can span years as families discover and rewatch content. Films like "Encanto" and "Frozen" sequels generate years of ongoing viewing as families discover the content through word of mouth or as children reach appropriate ages. This "library viewing" represents consistent baseline engagement between major releases and demonstrates the long-term value of Disney's content investments.

Seasonal content performs strongly on Disney+ as families seek entertainment aligned with holidays and special occasions. Holiday specials, Halloween-themed content, and summer releases align with family viewing patterns throughout the year, creating predictable spikes that advertisers can plan around. Advertisers can time campaigns around these seasonal viewing spikes to reach concentrated family audiences during moments when they're actively engaged with family entertainment.

Live events have begun appearing on Disney+, including some concert specials and premiere events that create must-watch moments beyond on-demand content. While live content remains limited compared to platforms like YouTube that have invested heavily in live streaming, Disney has experimented with live streaming to drive subscriber engagement and create the simultaneous viewing experiences that distinguish broadcast television.

Disney+ entered the advertising market in December 2022 with its ad-supported tier, fundamentally changing the platform's value proposition for advertisers who had previously had no access to Disney's streaming audience. This expansion has created new opportunities for brands seeking to reach family audiences through premium streaming content.

The ad-supported tier launched at $7.99 per month, pricing that has since been adjusted as Disney refined its strategy, offering a significant discount compared to the ad-free tier's premium pricing. This price difference encouraged new subscribers to accept advertising in exchange for savings, expanding Disney+'s addressable market to cost-conscious households. Existing subscribers could continue paying premium prices for ad-free viewing, preserving the experience for those willing to pay more.

Advertising on Disney+ commands premium CPMs reflecting the platform's brand-safe environment and engaged audiences who have chosen family-friendly content. CPMs typically range from $30-50+, higher than average streaming advertising rates, due to the quality of content and audience demographics that advertisers value. This premium pricing reflects Disney+'s differentiated positioning rather than simply reach metrics that would suggest lower rates.

Ad formats on Disney+ include standard video commercials similar to traditional television advertising, providing familiar creative formats that don't require specialized production. The platform has been conservative about ad load compared to free streaming services, typically running 4-5 minutes of advertising per hour to maintain viewer experience while monetizing ad-supported subscriptions. This restrained approach protects the viewing experience that attracts families to Disney+ in the first place.

Targeting capabilities on Disney+ include demographic targeting, geographic targeting, and some behavioral targeting based on viewing patterns that indicate household composition and interests. Advertisers can reach specific audience segments rather than buying broad inventory, improving efficiency compared to traditional television buying where waste was accepted as a cost of reaching valuable viewers.

Brand safety represents a key Disney+ advantage that justifies premium pricing for many advertisers. All content on the platform meets Disney's family-friendly standards, eliminating concerns about ads appearing alongside objectionable content that plague user-generated content platforms. This built-in brand safety appeals to risk-averse advertisers and family-focused brands that can't afford brand safety incidents.

For small businesses, accessing Disney+ advertising directly remains challenging due to minimum spend requirements and sales complexity that favor larger advertisers with dedicated media buying resources. Platforms like Adwave simplify access by including Disney+ inventory within broader streaming campaigns, allowing businesses to reach Disney+ audiences without dedicated Disney partnerships or minimum spend commitments.

Disney+'s 1.9% viewing share positions it distinctly within the competitive streaming landscape, demonstrating both the platform's strengths and the challenges of competing against services with broader content positioning.

YouTube dominates streaming viewership with approximately 10-11% of total TV viewing, nearly five times Disney+'s share, reflecting the platform's unmatched breadth of content. YouTube's content spans professional productions to user-generated videos to live streams, appealing to virtually all demographic groups with something for every interest and mood. Its advertising platform is also far more accessible to small businesses than Disney+'s premium offering, with self-service tools that enable campaigns at any budget level.

Netflix captures approximately 7-8% of TV viewing, roughly four times Disney+'s share, built on a massive content library developed over more than a decade of streaming leadership. Netflix's content spans every genre from prestige dramas to reality shows to documentaries, driving consistent viewing across all demographics rather than concentrating among specific audience segments. The platform's ad-supported tier, launched in 2022 shortly before Disney+, competes directly with Disney+ for advertiser budgets seeking premium streaming inventory.

Amazon Prime Video holds roughly 3-4% of viewing share, about twice Disney+'s, benefiting from integration with Amazon's broader Prime membership that provides streaming access as a bundled benefit. Amazon's combination of original content, licensed movies, and the Prime shipping bundle drives substantial viewing, though engagement varies significantly based on content releases because Prime Video lacks the franchise anchors that drive consistent Disney+ viewing.

Hulu, which Disney also owns and operates, captures around 3.4% of viewing, nearly double Disney+'s share despite sharing corporate parentage. Hulu's general entertainment positioning and extensive TV library attract adult viewers who watch more content overall than Disney+'s family-focused audience, demonstrating how Disney+ has intentionally sacrificed breadth for depth in serving specific audience segments.

Max, formerly HBO Max, competes at approximately 1.2-1.5% viewing share, slightly below Disney+ despite HBO's prestige content reputation. Max's programming attracts dedicated audiences seeking premium drama and documentary content but has struggled to match Disney+'s family appeal and franchise power that drive consistent engagement beyond hit releases.

Peacock, Paramount+, and other services each capture 1-2% of viewing, competing directly with Disney+ for streaming minutes in a fragmented middle tier of the market. The fragmented middle tier of streaming creates both competition and advertising opportunities across multiple platforms for advertisers seeking comprehensive reach.

Disney+'s audience composition differs substantially from general streaming platforms, creating unique advertising value for brands seeking to reach specific demographic segments efficiently.

Households with children represent Disney+'s core audience in ways that define the platform's advertising value proposition. Families with kids under 12 dramatically over-index on Disney+ usage compared to the general population, making the platform essential for advertisers targeting parents and children. For advertisers targeting these audiences, Disney+'s demographic concentration creates efficient reach unavailable on platforms with more diverse audiences where family households represent a minority of viewers.

Age demographics on Disney+ skew younger than overall streaming in ways that reflect the platform's content focus. While Netflix and Amazon attract viewers across all age groups fairly evenly, Disney+'s audience concentrates among children, parents of young children typically ages 25-45, and dedicated fans of Disney franchises who maintain viewing habits developed in childhood. This concentration means Disney+ delivers focused reach among family audiences rather than the diffuse reach of general-entertainment platforms.

Income demographics show Disney+ appealing across income levels, though the service over-indexes slightly among middle and upper-middle income households who can afford streaming subscriptions beyond basic entertainment needs. The subscription cost, even for the ad-supported tier, creates some barrier for lower-income households compared to free streaming alternatives like Tubi and Pluto TV that serve cost-conscious viewers.

Geographic distribution on Disney+ follows general streaming patterns, with strong suburban and urban presence reflecting broadband availability and demographic concentration. The service's family focus may create slightly higher usage in family-oriented suburban communities compared to urban centers with younger, childless populations who find less relevance in Disney+'s content library.

Viewing context on Disney+ often involves co-viewing, with parents and children watching together in shared family experiences. This co-viewing creates advertising exposure to multiple household members simultaneously, improving effective reach for family-oriented messaging that resonates with both parents making purchase decisions and children influencing those decisions.

Disney+'s trajectory from launch to current market position illustrates both the potential and challenges of building a streaming service in a mature, competitive market.

The service launched in November 2019 with immediate success driven by Disney's content library and aggressive launch pricing. The combination of beloved animated classics, Pixar films, Marvel movies, and Star Wars content created instant appeal that drove rapid subscriber acquisition. Disney's marketing power and brand recognition enabled launch-day subscriber numbers that validated the company's streaming strategy.

The COVID-19 pandemic accelerated Disney+ growth as homebound families sought entertainment options during lockdowns and social distancing. Parents particularly valued Disney+'s safe, trusted content during a stressful period when families spent unprecedented time together at home. By early 2022, Disney+ had reached over 130 million global subscribers, exceeding company projections and establishing the service as a major streaming player.

However, growth subsequently slowed as pandemic tailwinds faded and competition intensified across the streaming landscape. Subscriber counts have stabilized and slightly declined in some markets as Disney adjusted pricing and strategy to balance growth with profitability. The easy growth of the pandemic period gave way to harder work of retaining subscribers and attracting new ones in a saturated market.

Viewing share growth has followed a similar pattern to subscriber growth, with rapid gains followed by stabilization. Disney+ rapidly captured streaming share during 2020-2021, then plateaued around the 1.8-2.0% range as the service found its natural audience within the broader streaming market. The introduction of the ad-supported tier in late 2022 brought new subscribers but hasn't dramatically altered viewing share because many ad-supported subscribers were already watching through higher-priced tiers.

Looking forward, Disney+ faces several strategic challenges that will determine its future growth trajectory. Content costs for Marvel, Star Wars, and other franchises require massive investment to maintain release cadence that keeps subscribers engaged between major premieres. Competition from Netflix, Amazon, and Apple continues intensifying as deep-pocketed competitors invest billions in content acquisition. And the streaming market overall is maturing, making subscriber growth increasingly difficult as household penetration approaches saturation.

For advertisers, these dynamics suggest Disney+ will remain a valuable but specialized platform within broader streaming strategies. Its family audience and premium content environment will continue commanding premium pricing, while its viewing share likely remains in the 1.5-2.5% range absent major strategic changes that would alter its competitive positioning.

Netflix captures approximately four times more TV viewing than Disney+, with roughly 7-8% share compared to Disney+'s 1.9%. This gap reflects Netflix's broader content library, longer history, and appeal across all demographics rather than specific audience segments. Netflix targets general audiences with content ranging from prestige dramas to reality shows, while Disney+ focuses on family entertainment and franchise properties that limit its appeal to viewers outside those categories.

While children's content drives significant Disney+ viewing, adult fans of Marvel, Star Wars, and Pixar represent a substantial audience segment that watches for franchise content rather than family programming. The service attracts dedicated franchise fans who watch new series releases regardless of age, creating a dual audience of families and adult enthusiasts. However, households without children watch less Disney+ than the general streaming average, making the platform particularly valuable for family-focused advertisers rather than those targeting general adult audiences.

Small businesses can access Disney+ advertising through aggregated platforms like Adwave that include Disney+ inventory within broader streaming campaigns reaching multiple platforms simultaneously. Direct advertising through Disney requires substantial minimum commitments beyond most small business budgets because Disney's sales approach targets larger advertisers with bigger media investments. Aggregated approaches provide access starting at just $50 without dedicated Disney sales relationships that would require significant spending commitments.

Hulu's 3.4% viewing share exceeds Disney+'s 1.9% because Hulu targets adult audiences who watch more television overall than children and families. Adults have more available viewing time than households with children who balance TV with homework, activities, and early bedtimes. Additionally, Hulu's content library includes current TV series from broadcast networks, providing ongoing new content that drives regular viewing rather than the release-dependent patterns of Disney+'s franchise strategy.

"Bluey" consistently ranks among the most-watched streaming content across all platforms, driving substantial Disney+ viewing that extends well beyond its original children's target audience. Marvel series premieres generate significant viewership, particularly "Loki," "WandaVision," and other Marvel Cinematic Universe shows that attract adult fans alongside younger viewers. Classic Disney animated content generates steady family viewing throughout the year, providing baseline engagement between major franchise releases.

Nielsen Gauge and Media Distributor Gauge data provides the foundation for Disney+ viewing analysis throughout this article.

Disney+ captures approximately 1.9% of total television viewing in the United States as of mid-2025 according to Nielsen's monthly Gauge measurement, representing consistent performance throughout recent reporting periods.

The broader Disney company, including ESPN, FX, ABC, and other properties, commands 11.2% of total TV viewing as of December 2024, making Disney the largest media company by viewing share when considering its full portfolio of traditional and streaming properties.

"Bluey" on Disney+ accumulated 5.3 billion viewing minutes during December 2024, ranking as the second most-watched streaming title of the month across all platforms regardless of target demographic.

Disney+ launched its ad-supported tier in December 2022 at $7.99 per month, opening the platform to advertising for the first time in its history.

Combined, Disney's streaming services Disney+, Hulu, and ESPN+ capture approximately 6-7% of total TV viewing, comparable to Netflix alone when considered as a unified streaming offering.

Disney+ has grown to approximately 120 million global subscribers as of mid-2025, down from a peak of over 130 million in early 2022 as the company adjusted strategy following initial pandemic-driven growth.

YouTube leads streaming viewing with approximately 10-11% share, nearly five times Disney+'s viewing share.

Netflix captures approximately 7-8% of TV viewing, roughly four times Disney+'s share.

Disney+'s 1.9% viewing share represents just one piece of the streaming television landscape where advertisers can reach engaged audiences. Whether your target customers watch Disney+ with their families, stream Netflix dramas, or catch up on YouTube videos, television advertising offers powerful brand-building opportunities across platforms that can reach viewers wherever they choose to watch.

The fragmentation of viewing across multiple streaming services has made advertising access more complex but also more accessible for businesses of all sizes. Platforms like Adwave simplify multi-platform streaming advertising by providing access to 100+ premium channels, including Disney+, through a single campaign starting at just $50.

Ready to reach engaged audiences across Disney+ and other premium streaming platforms? See how Adwave works to create professional TV commercials and launch targeted campaigns that put your business on the biggest screen in your customers' homes.

Sources: Nielsen Gauge (2024-2025), Nielsen Media Distributor Gauge, Disney company reports

Last updated: July 2025